Throughout capital market history, only a small number of countries enter phases where all three pillars of long-term investment converge:

Data from 2025 indicates that Vietnam is now entering precisely such a convergence zone — a phase commonly referred to by global asset managers as the Pre-Emerging Market Expansion Phase, typically preceding large-scale institutional capital inflows.

This article analyzes Vietnam through three strategic lenses — GDP growth, market performance, and valuation — and explains why Vietnam is increasingly becoming a key destination in long-term global capital allocation.

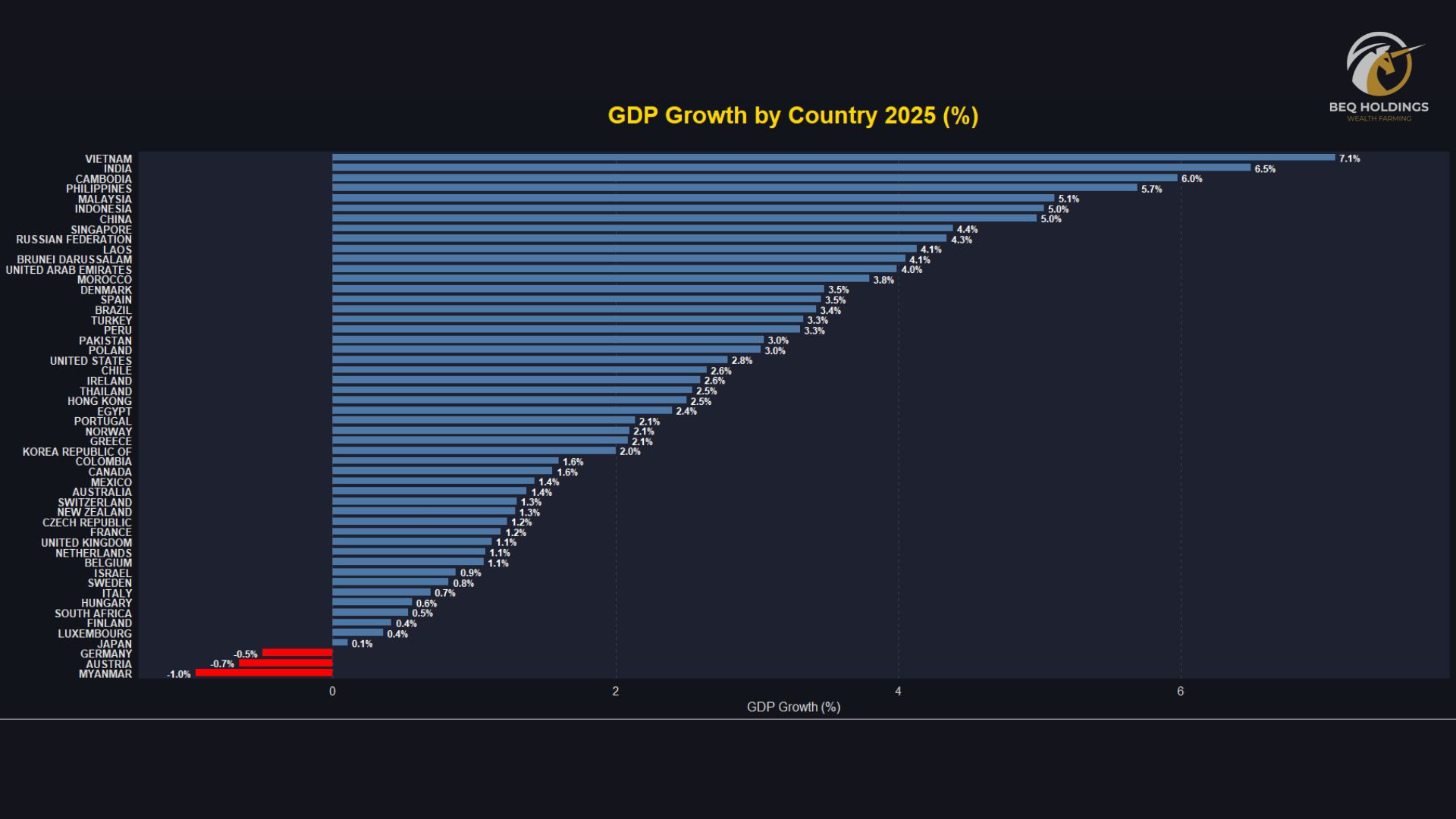

According to 2025 projections, Vietnam is expected to achieve 7.1% GDP growth, the highest among surveyed economies, exceeding:

Meanwhile, most developed economies remain near stagnation:

Structurally, high GDP growth drives:

In long-term valuation models, earnings growth is the primary determinant of multi-year index trajectories.

Markets sustaining GDP growth above 6% over multiple years often enter periods of:

Structural market re-rating and prolonged equity expansion cycles — especially when financial market depth and foreign participation increase.

Vietnam is now positioned firmly within this historical pattern.

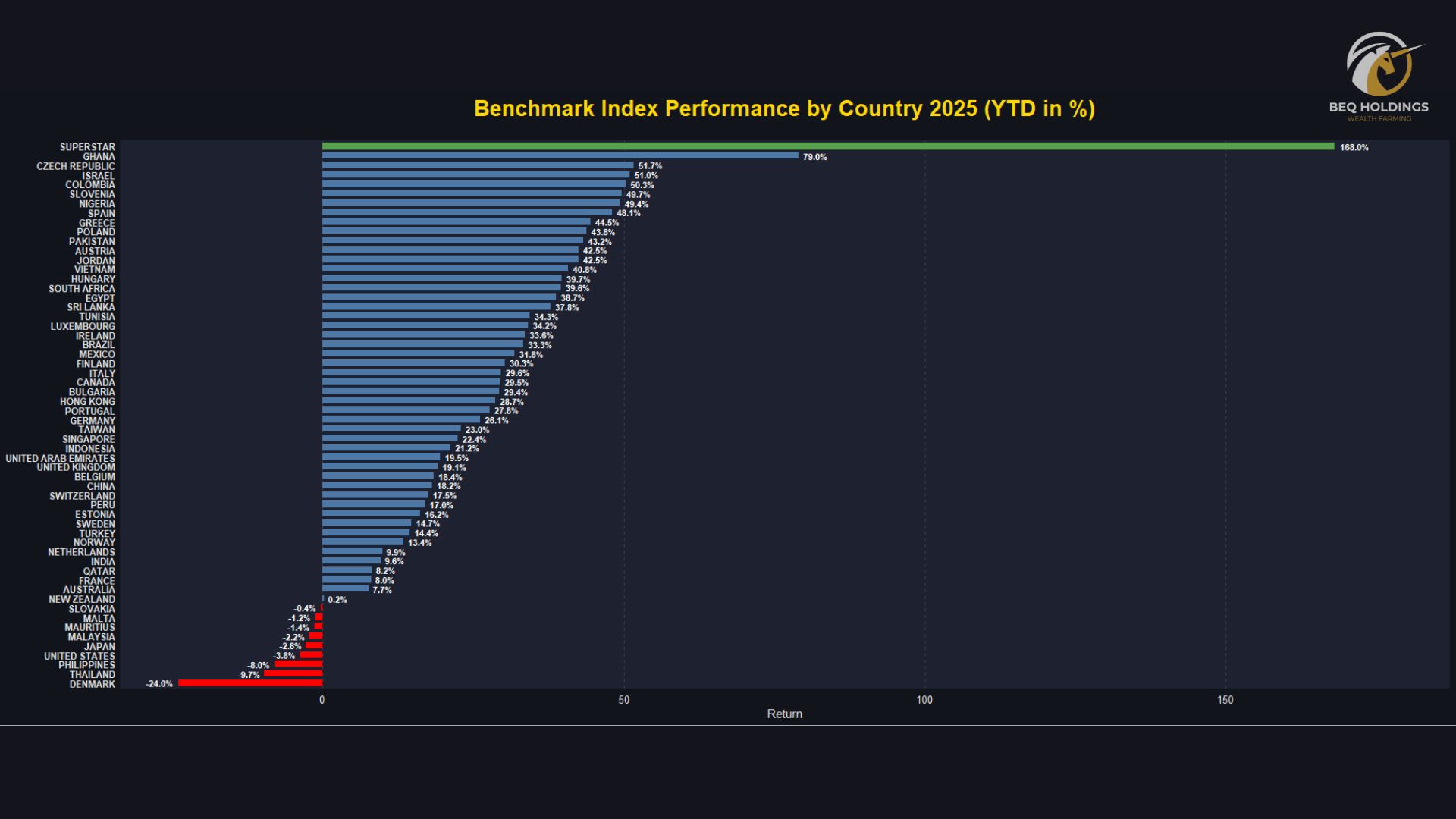

High growth must be validated by actual capital deployment.

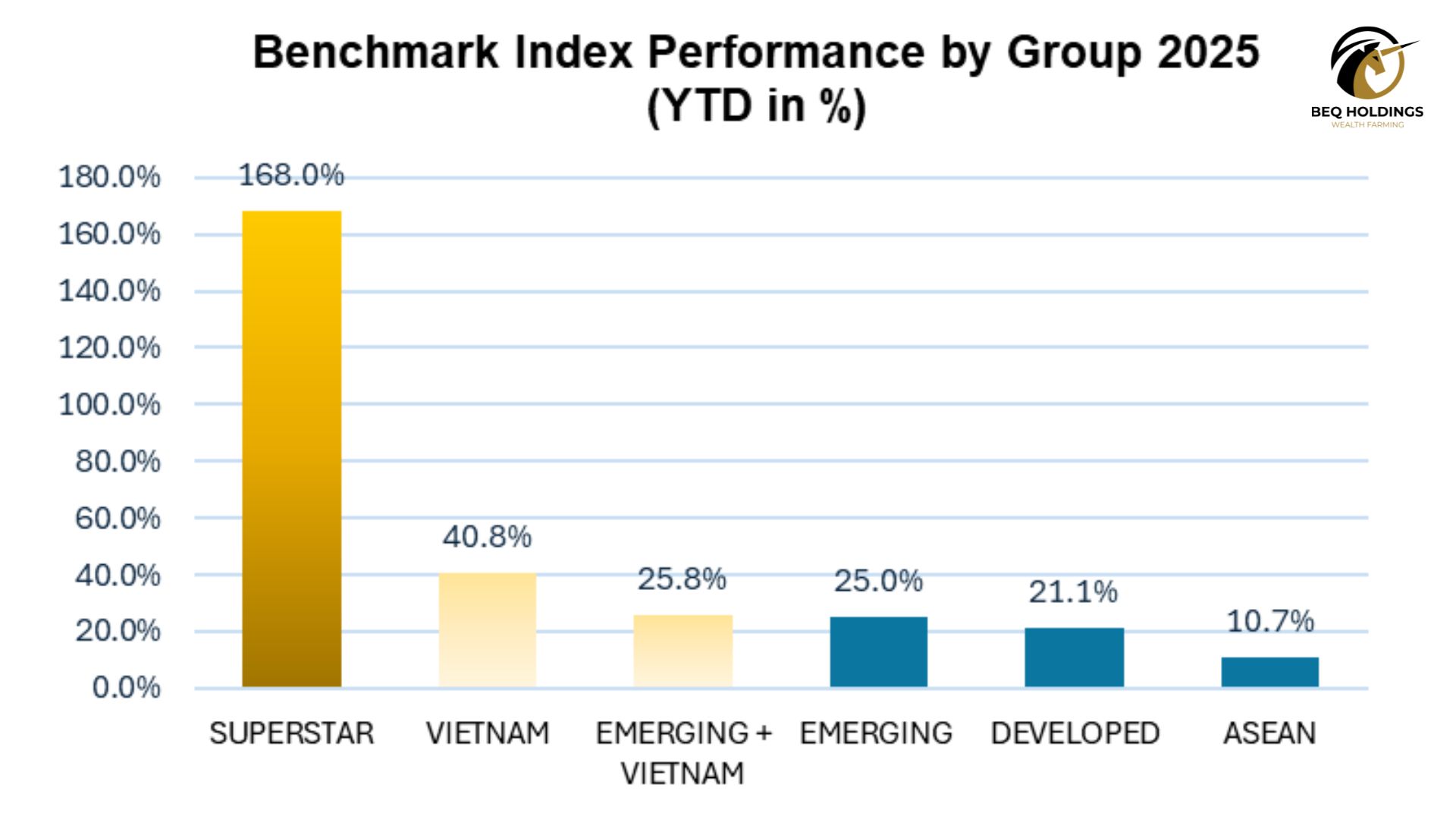

2025 year-to-date benchmark index performance shows:

Markets are now experiencing return dispersion, a classic early indicator of:

Capital rotation from mature markets into new growth economies.

Vietnam stands out because it combines:

In previous cycles across Korea, Taiwan, China, and India, early ETF and index-driven capital inflows were typically accompanied by outsized equity market returns relative to developed markets.

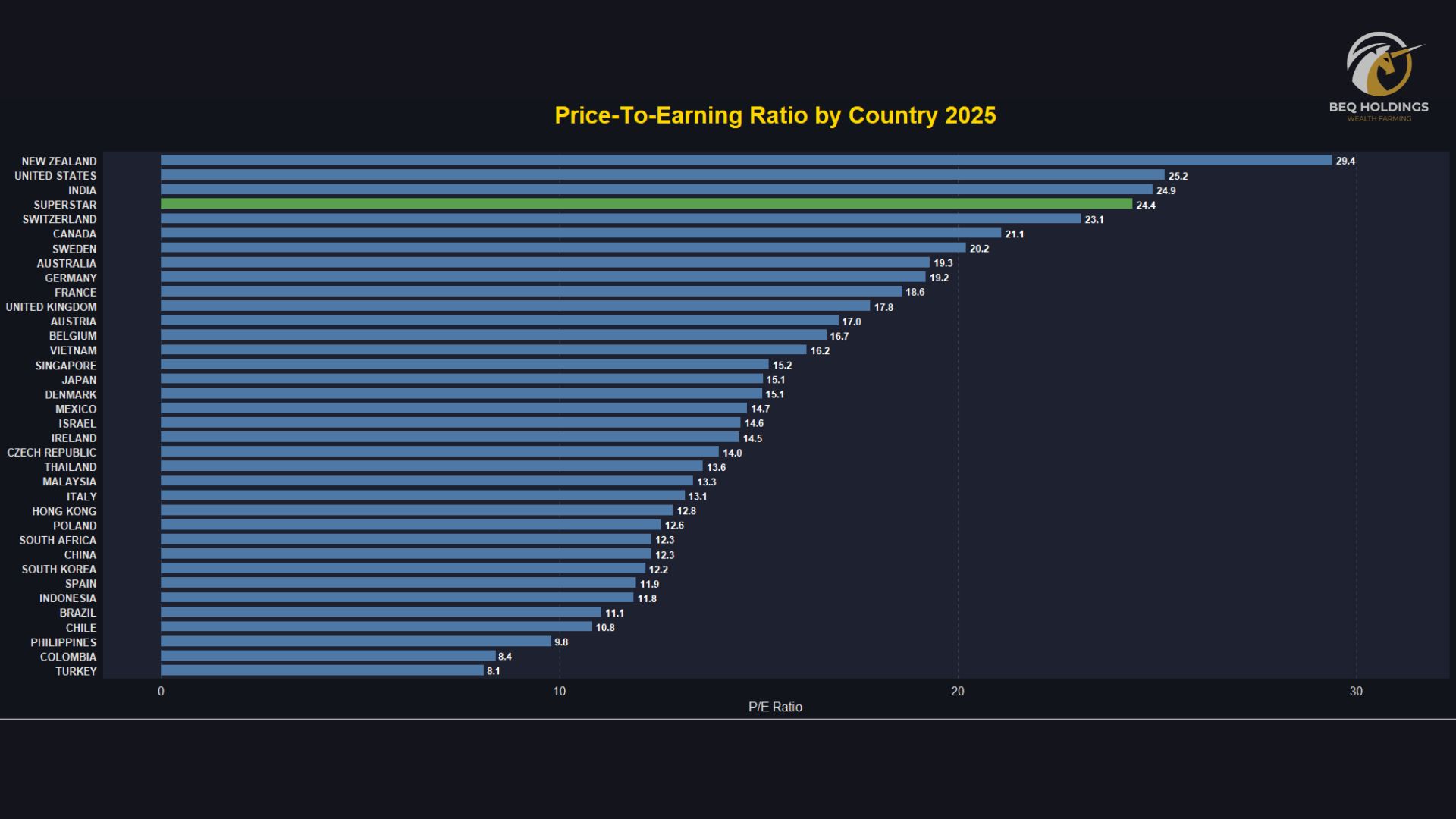

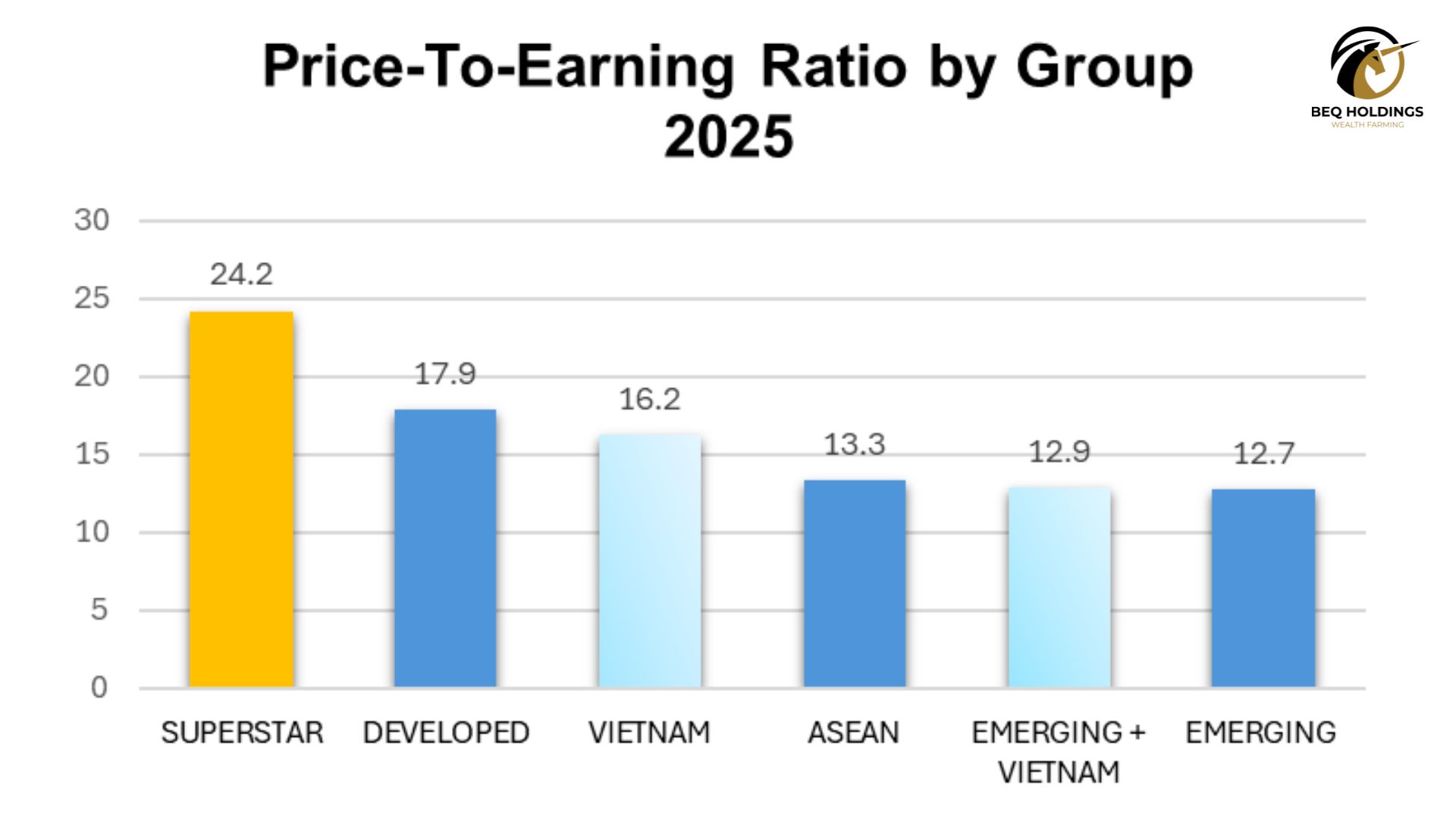

Despite strong performance, Vietnam’s 2025 market valuation remains moderate.

Price-to-Earnings Ratios:

While some emerging markets trade at lower multiples, they generally lack:

Vietnam is currently in a phase where:

Earnings growth precedes valuation multiple expansion

This is the optimal zone for long-term investors, where returns benefit from both:

Historically, such phases generate compounding return effects across multi-year investment horizons.

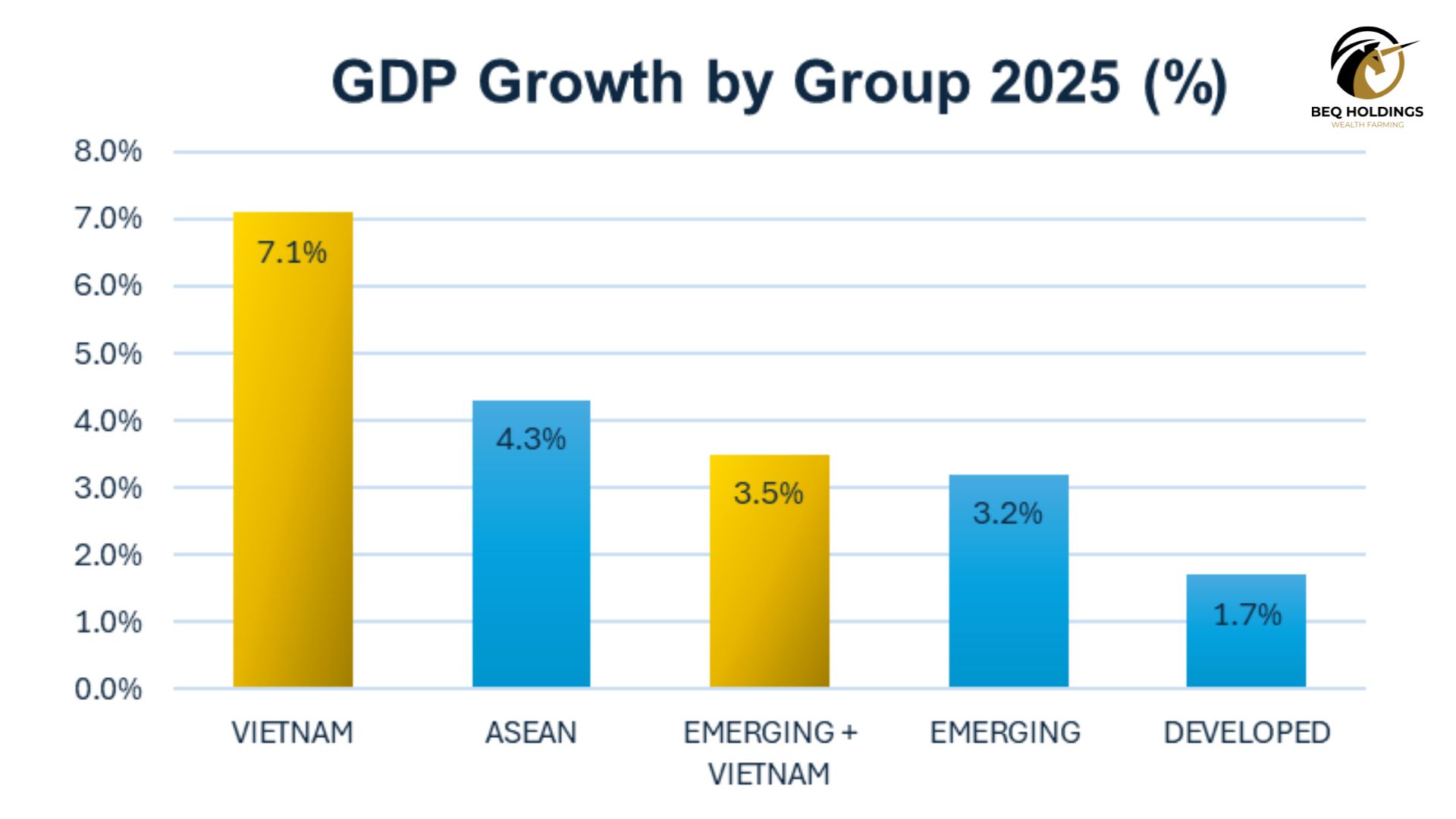

Group-level analysis further reinforces Vietnam’s positioning:

Vietnam is among the rare markets delivering:

This configuration strongly favors cycle-based and index-aligned asset allocation strategies, rather than short-term speculative positioning.

Global investment capital is now largely managed by:

These capital pools operate based on:

Therefore, when a market enters a growth and structural improvement phase, capital flows follow mechanical index-driven pathways, not discretionary sentiment.

This is why strategies such as:

are essential for investors seeking to participate in institutional capital cycles rather than short-term market noise.

As Vietnam enters a new global capital cycle, access to structured investment frameworks becomes increasingly critical.

BeQ Holdings operates as a WealthTech and Index Strategy ecosystem, focusing on:

Through CCPI – Cloud Computing Platform for Investment, BeQ enables investors to:

🎯 BeQ’s mission is not merely to provide investment products, but to build long-term, structured investment capability within emerging markets, where financial infrastructure often lags real economic development.

Looking ahead, Vietnam continues to benefit from:

These factors indicate that Vietnam’s capital market remains in the early phase of capitalization and liquidity expansion.

For institutional and strategic investors, this represents:

An optimal period to establish long-term exposure before full market repricing occurs.

Across multiple independent datasets:

Vietnam consistently emerges as one of the most compelling global emerging market investment destinations.

However, history also demonstrates that:

In this context, platforms such as BeQ Holdings and CCPI serve as critical bridges between:

Macroeconomic data, index-based strategies, institutional capital flows, and long-term wealth creation.

🌐 Index Strategy Tracking & Analytics Platform (CCPI):

👉 https://dashboardlite.ccpi.vn/login

🌐 BeQ Holdings Official Website:

👉 https://beqholdings.com/

📞 Hotline: +84 941 753 139

📧 Email: contact@beqholdings.com

Text box item sample content